There has been a lot of press recently on the growth of the catastrophe bond market. Investors, in particular pension funds, are jumping in seeking attractive yields and potentially greater diversification. How well do investors understand catastrophe bonds? Are they the “free lunch” they appear to be?

This post examines three aspects of catastrophe bonds:

-

Catastrophe bonds and how they work

-

Typical returns on catastrophe bonds

-

Risks

What are catastrophe bonds?

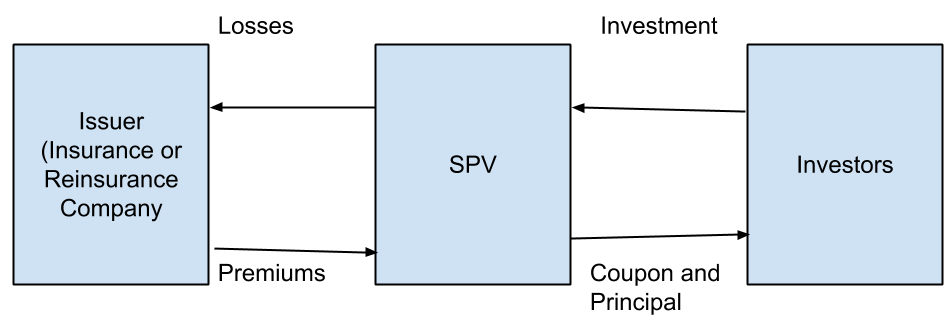

The proceeds from the sale of cat bonds are held in a special purpose vehicle (SPV) that invests these in high-grade securities. The issuer or sponsor (usually an insurance or reinsurance company) pays a premium to the SPV. The investor receives the return from the high-grade securities as well as the premium. At maturity the investor gets back their initial investment provided the insured events did not occur.

However if an insured event occurs, then the assets in the SPV are paid to the issuer to cover their losses. Investors will not get all or part of their investment back. The definition of the covered events and the calculation of the losses are documented at the outset. There are three typical trigger types: Indemnity, index or parametric.

Indemnity triggers are based on the actual losses of the issuer. While index triggers are based on losses reported by a specified third party. Parametric triggers are based on specific measures or functions of measures.

Indemnity triggers result in the lowest basis risk for the sponsor, however losses may take a long time to be calculated. Also with this approach modelling the probability and severity of losses requires a detailed understanding of the portfolio. Parametric triggers are more transparent from an investors perspective, but have higher basis risk for the sponsor.

The market has had strong growth in the past few years. There are currently around $19bn (USD) of catastrophe bonds outstanding. This is expected to hit $50bn in 2018 according to BNY Mellon.

Risk and return

The table below is from an article by RMS. It shows standard deviation and average return on some different asset classes.

The volatility for the Swiss Re Cat Bond Total Return Index is very low. The return for 10 year period shown is strong at around 8%. The average 1 year LIBOR rate over the last 10 years is about 2.5%. So the spread above LIBOR is around 5.5%. This seems very attractive. According this data, catastrophe bonds seem far superior to any of the other investments assets shown in the table.

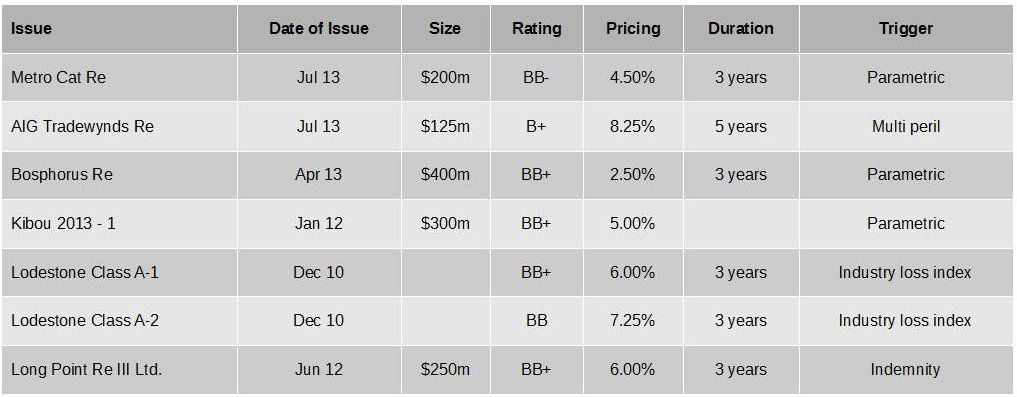

Examples of catastrophe bonds issued

A series arranged by Swiss Re (covering The Travelers Indemnity Company) is rated at BB+ and has a spread of 6% over Treasury money market funds. The issue is under Long Point Re in the table below. For further details see presentation by Swiss Re.

The average spread on a the BofA Merrill Lynch US Corporate BB Index at the issue date is around 5%. This gives an additional 1% over a similarly rated corporate bond.

The table below summarises some recent deals and give an idea of the returns on offer. The data is source from Artemis’ website. Pricing is the spread over the yield on collateral held. This is usually Treasury money market securities.

The returns on catastrophe bonds have reduced over time as investor demand has increased. From reading about some of the issues, it is not uncommon for the yield to come in lower than initially indicated.

The key risks are:

-

Credit risk on the collateral held, as well as counterparty credit risk from hedging and other transactions.

-

Insurance risk from the event occurring.

-

Model risk

Model risk is easy to underestimate. Investors need to rely on either in-house or third-party modeller to help set the price. However models can have limitations particularly when modelling extreme events such as catastrophes.

Any default in the pool of collateral assets will reduce returns to investors. Another related risk is counterparty credit risk. At the time of its collapse, Lehman Brothers was the provider of swaps to 4 live catastrophe bonds according to RMS.

Insurance risk is quantified using complex modelling. Investors rely on one of the following to help understand and quantify the risk: the sponsoring issuer, a rating agency or specialist advisor.

The GFC highlighted the dangers of assets where investors did not understand the underlying risks. While I am not saying that catastrophe bonds can precipitate another GFC, some of the features are:

-

A complex product with complex underlying risk

-

Investors who do not have the information and skills to model the risk

-

Reliance on models

-

Sponsors and advisors have a possible conflict of interest

-

Low interest environment where alternative investments with higher returns are attractive.

Conclusion

As the BNY Mellon report notes, the size of catastrophe bonds on issue looks set to grow exponentially. These products give an alternative to off load and manage the risks from catastrophes for insurers and reinsurers. For investors the high yields on offer and the lack of correlation to other financial assets make these highly attractive. However the nature of the product is unusual, in particular, measurement of risks is uncertain and difficult.

References and links

LIBOR average rates can be found here.

For data on bond indices click here.

Great read, Sen. I like how you focus on the issues that might affect an investor in cat bonds, as opposed to from an issuer’s perspective- ie as an interesting alternative to traditional reinsurance.

Two factors that I think might mitigate the dangers that cat bond investors are exposed to:

-basis risk works in investors’ favour since triggers are so narrowly defined (apparently, only one in nine cat bonds sold in the gulf region were paid out after hurricane Katrina)

-public opinion seems to acknowledge that 100-year floods are becoming more and more prevalent due to global warming. This might bias investors towards being more conservative in their exposure to extreme weather risk.

Hi Matt,

Thank you very much for your comments. Agree with both your points. With your first point, a large number of bonds have parametric triggers which are more transparent from the investors perspective. However as you note it is less in the insurer’s favour.

On the second point. I think there is growing awareness on quantifying probabilities and the judgement required to deal with uncertainty in the modelling. How sure are you this is a 1 in 100 event rather than say 1 in 20 years? To date a lot of the cat bonds (around 70% on issue if I recall correctly) tend to be US wind perils which have a lot more data and modelling to support pricing.

Regards,

Sen.