Economics of automation and robotics

Automation and robotics are the buzzwords in industry right now. While robotics has been around in manufacturing, white-collar jobs are now starting to be automated. Financial services firms in Australia want to take out cost, improve quality and reduce risk using automation.

For the ordinary person on the street, the question is whether they and their children will have jobs in the future. Or will the introduction of robotics and automation allow us to stop doing the mundane parts of our jobs and focus on the interesting parts such as creation, socialisation, etc?

What does it mean for the investor? Robotics have allowed companies to produce more, at better quality, and at a lower cost. While some businesses and industries did not survive, investors (and society) have benefited through productivity gains.

Trends in Australian home loan interest rates

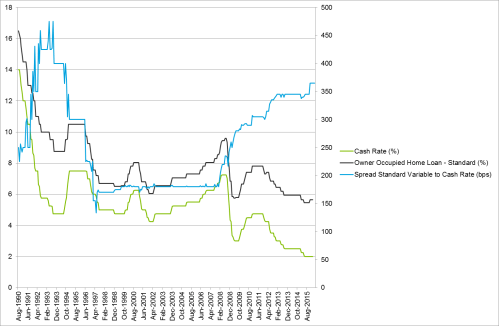

The reserve bank of Australia’s decision to cut interest by 0.25% in May brings the cash rate to an all-time low. Three of the Big 4 followed by cutting their standard variable rate (SVR) by 0.25%. Only ANZ passed on 0.19% citing higher funding costs.

The RBA publishes a range of interest rate statistics including the mortgage standard variable rate and discounted mortgage rate, by both for major lenders and regional lenders. Here are some observations from a quick analysis of the RBA interest rate data.

For a number of years from the late 1990s to just before the GFC, banks moved their head line standard variable rate (SVR) lock step with the RBA cash rate. Following the GFC, banks did not pass on all the decreases to the cash rate as their funding spreads widened. The chart shows that the gap between the cash rate and the headline standard variable rate increased from around 175bps to over 350bps, particularly from around the GFC. With the banks following the RBA’s May lead, the headline SVR is also at its lowest.

Showing the headline standard variable rate however does not show the full picture. Some borrowers do not pay the full standard variable rate. For example simply taking up one of the banking packages e.g. CBA’s Wealth Package, will give a borrower a reasonable discount (around 0.7%).

The RBA also publishes a series of discounted variable rates offered. The chart below shows the discounted variable rate on owner occupied loans.

Since 2008, the level of discounts offered by banks to mortgage clients have increased by around 20bps. One factor could be selective pricing based on risk, rather than on overall reduction in the headline SVR. However even spread on the discounted SVR over the cash rate has increased significantly, despite accounting for a greater level of discounting.

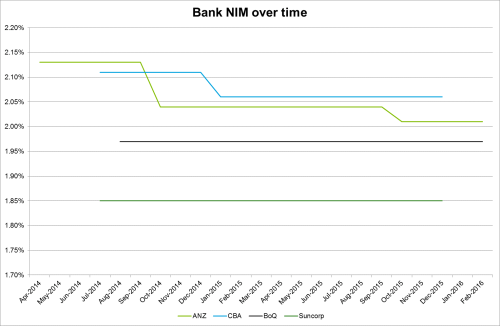

At least over the past 18 months, the NIM for most banks has been steady. I have had a look at the net interest margin of two big 4 banks (ANZ, CBA) and two majors (Suncorp, and Adelaide Bendigo) from their annual reports. ANZ did recently show a 3bps reduction in their NIM. Interestingly Westpac who also reported half year results recently showed a 3 bps increase in NIM, through better pricing on customer deposits.

At least for the time being it seems like the banks have been able to pass on lower interest rates while more or less maintaining margins. For home owners, lower interest rates are bonus. Whether the lower interest rates have the RBAs’ desired effect remains to be seen.

Source of data:

Stress testing and its Cold War genesis

The creative apocalypse that wasn’t

While not related to financial services, this article by Steven Johnson is an interesting read. It looks at digital technology has changed creative industries. At the heart of this is the question of how the risk return balance changed in the digital era. For example, is a mid budget independently produced movie a better or worse risk in the age of Netflix compared to 10 years ago? Are you more likely to sink money to produce such a movie?

The asset management industry and financial stability

The topic of whether or not Australian banks are well capitalised has been running hot. However the asset management sector has largely gone unnoticed when talking about financial system stability. In Australia, total assets held by asset managers (including superannuation funds, insurers and units trusts) are 75% of the assets held by banks. In fact the burning question at the moment when talking about asset management seems to be whether or not you need $1m to have a comfortable retirement. In addition, industry professionals vent plenty of frustration when talking about the apathy the Australian population seems to have towards saving for retirement. However this apathy could be one of the factors that mitigate the systemic risk from the asset management sector, according to this informative article from the RBA. (more…)

The role of the regulator and risk culture

Recently Paul Fisher of the PRA gave a speech titled “Regulation and future of the insurance industry“. In it he says:

“Solvency II will introduce an enhanced system of governance standards – promoting the embedding of a strong risk culture, demonstrable within the day-to-day operations of insurers.”

Risk culture is big in risk management now. Prudential regulations started off being directive based, then evolved to principles based regulation. Post GFC we have beyond principles to risk culture. While companies and consultants talk about it, it is an ethereal concept.

A system of governance standards is certainly very useful as it gives a common set of principles for risk processes, policies and reporting that should exist. Rules and limits are also useful where management have requirements that are NOT subject to personal judgement. But can you “implement” risk culture?

To me risk culture exists where the organisation and people value and exercise traits such as prudence, inquiry, transparency and critical thinking. Risk culture makes standards effective. Sure, standards can help with risk culture by requiring that people do things like getting models reviewed and approved. However if people do these things only because of standards then the standards haven’t really created good risk culture…

What is a Board to do?

According to the latest paper on governance from the Basel Committee, “Board members have responsibilities to the bank’s overall interests, regardless of who appoints them.” What does this mean? What are the bank’s “overall interests”? Board members are elected by the shareholders and are there to represent their interests – right? This statement seems to suggest that the authors believe there will be situations where the “overall interests” and shareholders’ interests diverge.

Exploring risk based pricing for corporate loans

Previously I wrote about an approach to pricing loans, where the spread is set to cover expected losses from default, and to make a return on capital allocated. In this article I use the framework to explore the drivers of credit spreads that banks would calculate if they used the Basel IRB formula to calculate the amount of capital required.

Some banks may use regulatory capital to derive capital as this reflects the amount of regulatory capital required for the loan. The regulatory approach as specified by BCBS captures key drivers of risk such as probability of default, loss given default, systemic risk, and term.

This simple pricing approach reveals some interesting dynamics of the required credit spread. For example, with higher rated securities, the spread is driven by capital requirements and not the expected loss. Drivers of capital such as correlation between defaults and term to maturity have a larger influence.

Risk based pricing of loans by banks

Introduction

In an earlier post, I talked about how banks set interest rates for loans compared to investors. I would like to explore the bank’s approach over a couple of posts. This post covers one approach to setting the interest rate to charge for a corporate loan.

The interest rate charged is:

- The cost of borrowing funds

- Expected cost of loan default

- Expense margin

- A rate of return on capital employed

Components of interest rate

Sound capital planning practices according to the Basel Committee

The Basel Committee on Banking Supervision (BCBS) released a paper titled “A Sound Capital Planning Process: Fundamental Elements” in January 2014. This paper does not propose changes to standards or capital requirements. Instead, it reports on a study carried out by BCBS on the capital planning process at a number of banks.

The paper has a good overview of what is good capital planning and is worth reading if you work in bank capital management. It covers the following fundamental elements: internal control and governance, capital policy and risk capture, forward-looking view and management framework for preserving capital.

Banks must forecast future capital needs under a range of conditions as part of their internal capital adequacy assessment process (ICAAP). ICAAP is an part of Basel 2, Pillar 2 requirements. The BCBS document “Enhancements to the Basel II framework” outlined measures to strengthen Pillar 2 requirements. For Australian banks, the requirements are set out in Australian Prudential Regulation Authority’s standards and practice guides (APS 110 and CPG 110 respectively).

A number of the components of a sound capital planning process are already requirements under the current standards or guidance that Australian banks need to follow. (more…)