Introduction

In an earlier post, I talked about how banks set interest rates for loans compared to investors. I would like to explore the bank’s approach over a couple of posts. This post covers one approach to setting the interest rate to charge for a corporate loan.

The interest rate charged is:

- The cost of borrowing funds

- Expected cost of loan default

- Expense margin

- A rate of return on capital employed

Components of interest rate

The cost of borrowing funds reflects the cost that the bank pays to borrow money. Banks have an allocation mechanism to allocate cost of funds down to the loans in the portfolio.

Expected loss is PD x LGD x EAD, and is relatively straight forward. The components are Probability of Default (PD), Loss Given Default (LGD) and Exposure at Default (EAD). The PD, LGD and EAD need to be estimated using credit risk models.

Cost of capital is the internal capital allocation multiplied by hurdle rate. A common practice is to use economic capital as the internal capital measure. However smaller, less sophisticated banks may use a regulatory capital approach. The section below covers economic capital in more detail.

In addition, the bank may charge a margin for expenses. For large loans such as in the institutional space, this will be a very small component. This and the cost of funds are not considered further in this article.

Economic capital and cost of capital

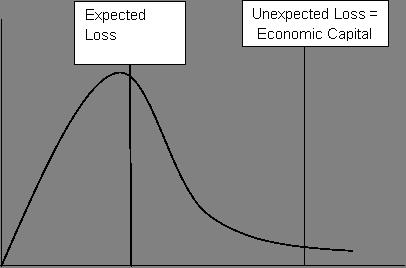

Economic capital is also known as unexpected loss. Note that there are differences in terminology that people use. In some contexts unexpected loss is the standard deviation. In other instances, this is the potential loss that capital is held for. The latter is used as a measure of risk based capital. Of course actual capital held will be different.

Economic capital is generally calculated using a VaR approach. That is, the loss at given level of probability, known as the confidence level. This is illustrated in the diagram below:

To calculate it, banks need a model of the distribution of losses from all different risks. For credit risk a bank will have a model of the loan portfolio with the following key drivers:

- PD of each borrower

- LGD of each facility

- EAD of each facility / borrower

- Correlation or dependence between borrowers

- Rating transitions

Two banks can produce vastly different costs of capital on the same loan due to:

- Difference in the internal capital model they use and the estimates for the different drivers and inputs. Some banks may use regulatory capital consumed.

- Confidence level chosen

- Other risks that the company runs, and how much capital is assigned to cover these.

- Hurdle rate.

The next two paragraphs expand on the hurdle rate and confidence level.

Hurdle rate: This is the return that the bank needs to make on the capital employed. It is calculated using CAPM or WACC. This is firm specific, both as the model inputs are subjective and as each firm will have different results.

Confidence level: This is generally set as part of the bank’s risk appetite or target probability of default.

Conclusion

The approach described above is considered good, if not best practice for loan pricing in banks. While banks may move away from the risk based price e.g. for strategic reasons, this should be computed. This ensures that the expected default cost along with a sufficient return on capital utilised is priced in. The approach requires the development of models to calculate the economic capital as well as credit risk factors such as PD and LGD.

I would like to develop this further, but I will leave it for another post!

[…] Risk based pricing of loans by banks […]