Previously I wrote about an approach to pricing loans, where the spread is set to cover expected losses from default, and to make a return on capital allocated. In this article I use the framework to explore the drivers of credit spreads that banks would calculate if they used the Basel IRB formula to calculate the amount of capital required.

Some banks may use regulatory capital to derive capital as this reflects the amount of regulatory capital required for the loan. The regulatory approach as specified by BCBS captures key drivers of risk such as probability of default, loss given default, systemic risk, and term.

This simple pricing approach reveals some interesting dynamics of the required credit spread. For example, with higher rated securities, the spread is driven by capital requirements and not the expected loss. Drivers of capital such as correlation between defaults and term to maturity have a larger influence.

Credit risk capital

The Basel internal rating based (IRB) formula is based on a one factor credit portfolio model. A note on the Basel IRB formula can be found here. Large banks will run their own portfolio credit models that capture more of the dynamics of credit portfolios. More complex internal models can capture diversification and single concentration effects that the Basel IRB formula does not.

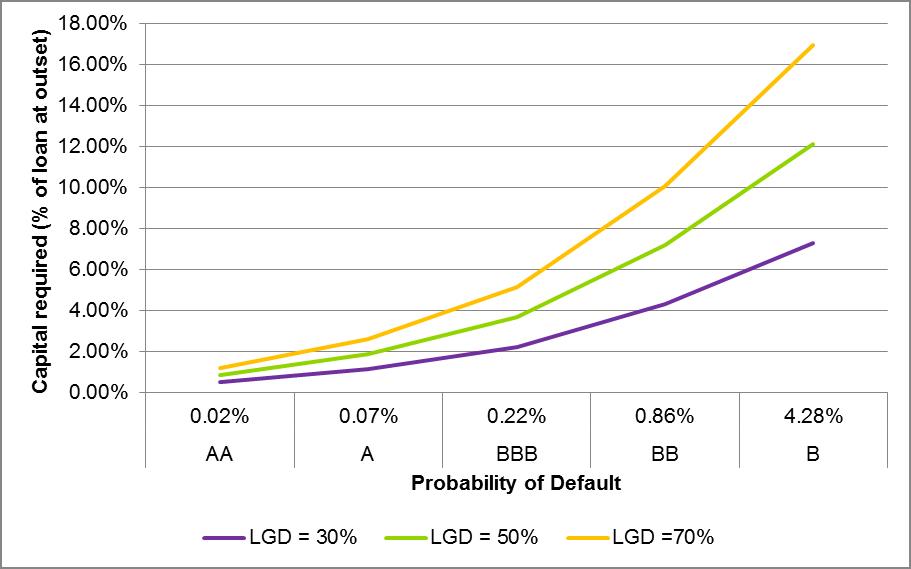

To get an idea of capital required, the table below shows capital held for different Standards and Poor’s ratings grades. To provide some context the Probability of Default (PD) is set equal to default rates observed by S&P for different credit grades from S&P’s 2013 default study. The chart shows capital expressed as a percentage of the loan amount at the outset by PD for three (Loss Given Default) LGD estimates:

Note I have used a loan term of 2 years. The IRB formula uses “downturn” LGD. The reason for this is that there is correlation between the PD and LGD. The use of “downturn” estimates implicitly captures this correlation.

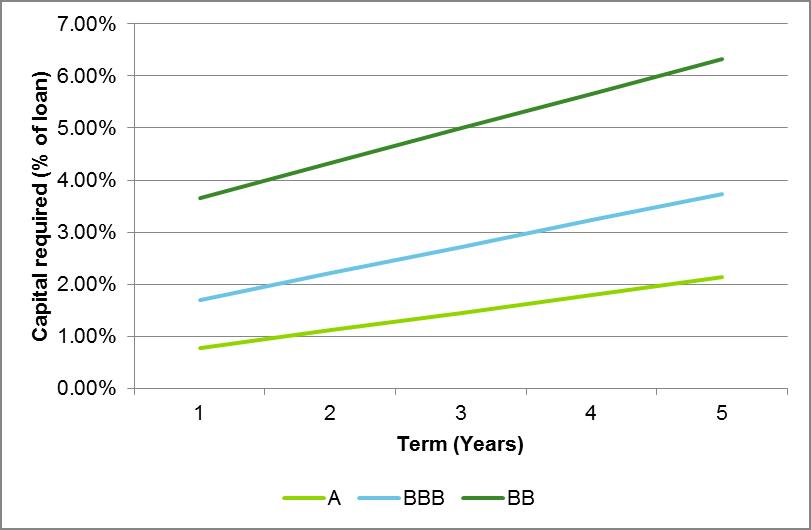

The chart below shows how capital varies by loan term.

(Calculated with an LGD of 30%)

Capital for other risk types

Capital also needs to be held for other risks that the bank faces when lending money to clients. This includes operational risk. It could also include market risk, if the bank has interest rate risk from funding the loan without matching exactly.

I have assumed that capital required for the other risk types is 25% of the credit risk capital. I.e. the capital requirements of the bank can be split 80% credit risk and 20% other risks.

Cost of capital

Once the capital requirement is known, a cost of capital rate is applied. Assume that the cost of capital rate is 12%.

Credit Spreads

Credit spreads required in pricing cover the cost of capital, as well as, the expected cost of default and any margins for expenses. This is added to the cost of funding the loan for the bank.

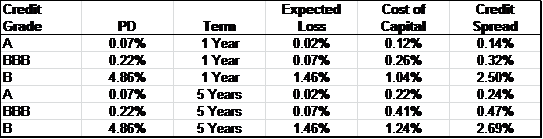

The table below builds up the spread required for different credit grades. I have not added an expense margin. The expense margin will vary depending on the size of the loan, cost structure of the bank or the division selling the loan and perhaps the sales channel.

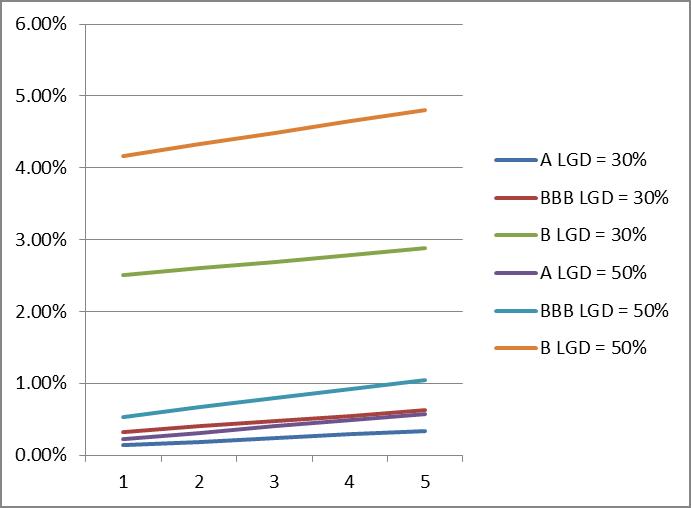

The graph shows final spreads for combinations of PD grade, LGD estimate and terms to maturity (horizontal axis):

Some Observations

- Higher risk means higher credit spreads, obviously. The relationship between spread and downturn LGD is linear. However the relationship is not linear for PD.

- The relationship between the capital and maturity is linear. This is a feature of the Basel IRB formula. The slope depends on the PD.

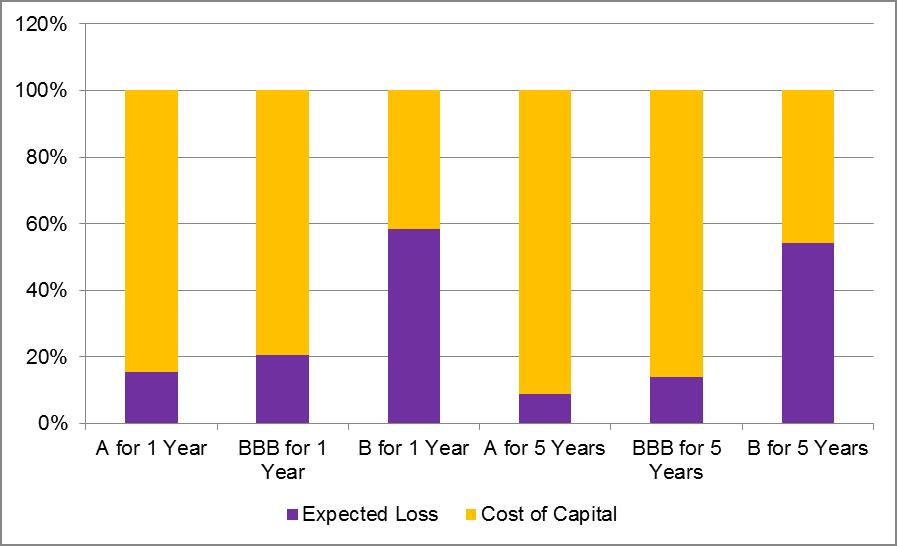

- An interesting observation is the relative contribution of the expected loss and the cost of capital to the spread. For highly rated securities, the expected loss is a minor part. However for lower rated securities, this dominates. The credit portfolio model that determines capital allocation becomes more important for highly rated securities relative to the expected cost (driven by PD and LGD). The graph below shows the relative contribution. For highly rated securities in this example the correlation to the systemic risk factor becomes a more important driver.

- Term to maturity influences required credit spread for higher rate securities.

Conclusion

This fairly simple model highlights some interesting dynamics of how risk can impact the pricing of corporate loans. While the approach and thinking is similar to how a bank might approach the pricing, there are still a number of complexities to overcome. Least of which is coming up with estimates for PD and LGD. Then there are challenges of how to compete in the market, practices and incentives for the sales channel, etc.